Alphabet Inc. on Bitunix: How to Trade GOOGLUSDT

Learn what Alphabet is and how to trade GOOGLUSDT on Bitunix. Explore Google stock forecast themes, Alphabet AI stock narratives, earnings catalysts, and beginner trading basics.

Decentralized finance reimagined how markets work. Instead of matching buyers and sellers through a central order book, many decentralized exchanges rely on liquidity pools that quote prices automatically. This choice did not happen by accident. It solved a set of problems that on-chain order books struggled with, such as thin liquidity, high gas cost, and the need for ultra fast matching engines.

This guide explains order books vs liquidity pools with plain language and detailed examples. You will learn how order book trading sets prices, how automated market makers quote trades from a pool, why DeFi liquidity models favor pools, and when an order book still makes sense.

[ez-toc]

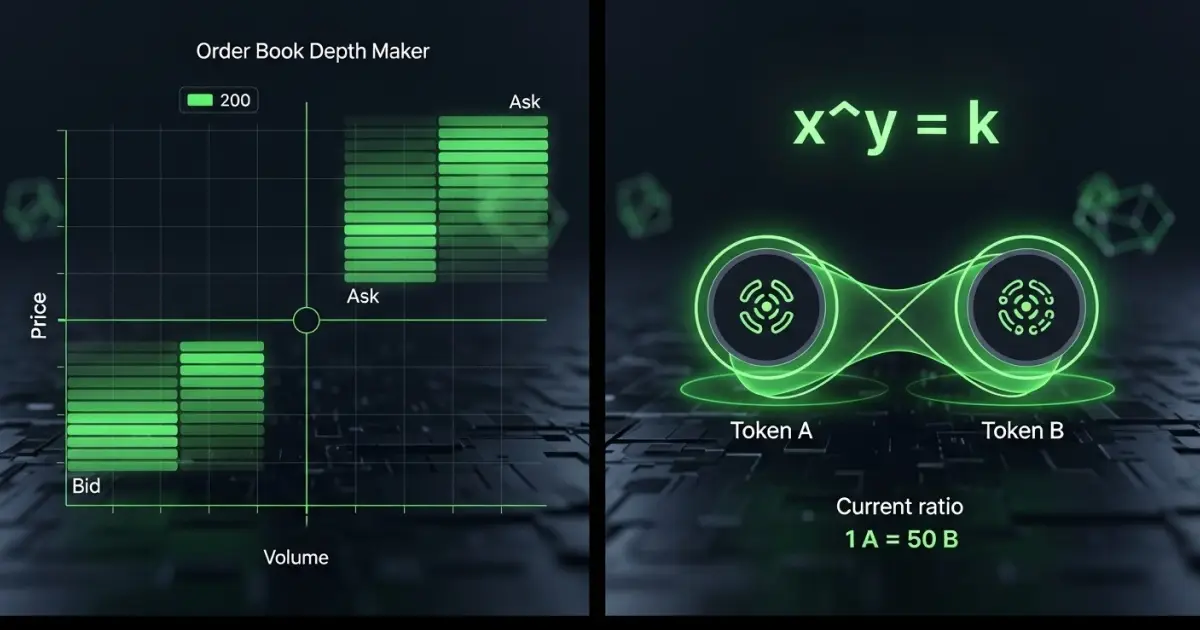

An order book is a list of buy and sell orders for a particular asset. Each order specifies a price and a quantity. The order book displays these buy and sell orders, facilitating trading activities by matching buyers and sellers for the asset. The best bid is the highest price someone will pay. The best ask is the lowest price someone will sell. The difference between them is the spread. When a new order arrives, a matching engine compares it to the current book. If there is a compatible order on the other side, the engine executes a trade and removes or updates the filled orders.

Characteristics of order book trading:

Order books can face challenges in illiquid markets or when there are low trading volumes, which can result in higher slippage and decreased efficiency in executing trades.

Order books dominate in traditional finance and on traditional centralized exchanges because those platforms can operate high performance servers and maintain custody of balances while orders rest. Traditional centralized exchanges use order books to match buy and sell orders for specific assets, providing transparency and efficient execution for a wide range of trading activities.

A liquidity pool is a smart contract that holds reserves of two tokens and quotes a price based on an algorithm. This is how liquidity pools work: users provide liquidity by depositing assets into the pool, and the assets deposited are then used to facilitate trades between other users. Anyone can deposit equal values of the two tokens into the pool and become a liquidity provider. In return, they receive a share of trading fees and are also issued LP tokens representing their share of the assets deposited. The pool does not need to search for a counterparty. It is the counterparty.

Why this matters on-chain:

This model gave DeFi a practical way to build markets while keeping custody with users.

The automated market maker or AMM, also known as automated market makers (AMMs), is the algorithm that a pool uses to quote prices and facilitate trades. AMMs automatically set the exchange rate for token swaps based on the current reserves in the liquidity pool, eliminating the need for traditional order books. This mechanism enables efficient and continuous trading by allowing users to swap tokens directly with the pool.

In section 3.1, AMMs do not require matching buyers and sellers, which allows for seamless token swaps at any time, regardless of market participant activity.

The first popular design used the rule x · y = k, where x and y are the token reserves and k is constant. If a trader buys token X, the pool’s X reserve decreases and the price rises because the product must remain constant. The more you buy in one transaction, the higher the price you pay. This is price impact. The fee that the trader pays stays in the pool and compensates liquidity providers.

Properties:

Stablecoin pairs or assets that track each other, such as USDC and DAI, benefit from a different curve. A stableswap AMM keeps the price near one while still allowing large trades with very low slippage. It does this by blending a constant sum region around the peg with a constant product region away from the peg.

Properties:

Uniswap V3 introduced concentrated liquidity. Liquidity providers choose specific price ranges where their funds are active, concentrating their assets within those intervals. Inside the selected range, trades use only the liquidity allocated there. This increases capital efficiency because funds are not spread across prices that rarely occur. If the market price leaves your range, your position stops earning fees until you rebalance.

Properties:

These DeFi liquidity models power most decentralized exchanges today.

| Feature | Order Book Trading | Liquidity Pools Explained |

| Counterparty | Another trader’s order | The pool itself |

| Price formation | Bids and asks placed by traders and market makers | Algorithmic pricing from reserves and an AMM curve |

| Capital source | Market makers and resting orders | Liquidity providers deposit funds |

| Settlement | Matching engine, often off-chain, finalizes then updates balances | Single on-chain transaction updates pool and balances |

| Trading pairs | Supports a wide range of trading pairs, typically curated for liquidity and market demand | Enables a variety of trading pairs, including long-tail or permissionless pairs, often without centralized approval |

| Best for | Mature markets with deep liquidity, complex order types, derivatives | On-chain spot swaps, long tail tokens, permissionless market making |

| Main costs | Spread, taker fees, maker fees, funding for leverage | Price impact, swap fee, gas, impermanent loss for LPs |

| Primary risks | Custody on a centralized exchange, order book spoofing, exchange downtime | Smart contract risk, MEV, impermanent loss, oracle issues for hybrids |

Blockchains do not handle millions of order updates per second. Each update costs gas, and every cancel or refresh is a transaction. Early attempts at on-chain order books suffered from massive overhead, poor user experience, and thin books. Liquidity pools solved these issues in several ways. Decentralized exchanges (DEXs) and DeFi platforms use liquidity pools as a core mechanism to facilitate trading and liquidity provision. Decentralized finance (DeFi) and the broader DeFi ecosystem rely on these innovations to enable decentralized trading, allowing users to trade directly from their wallets without intermediaries.

Anyone can become a liquidity provider by depositing assets. This crowdsources market making and avoids the need to recruit professional firms.

A swap happens in one transaction. There is no risk of orders resting in the book without being matched.

Pools are smart contracts that other contracts can integrate with. Lending protocols, yield vaults, and aggregators all plug into AMMs. This is core to the DeFi design philosophy.

An AMM requires only token transfers and math on reserves. The chain handles ordering. There is no separate matching engine to operate.

Because liquidity and pricing live on-chain, as long as the network is live, the market can operate.

Liquidity pools are fundamental to the growth and accessibility of the crypto market, allowing users to participate in decentralized finance (DeFi) without intermediaries and supporting the ongoing innovation of the DeFi ecosystem.

These advantages explain why DeFi uses liquidity pools for most spot trading. Decentralized exchanges, as a key part of decentralized finance DeFi, leverage these pools to enable decentralized trading and empower users within the crypto market.

Providing liquidity involves certain risks, including impermanent loss and smart contract vulnerabilities.

Order books discover price from human or algorithmic intent expressed as limit orders. If many buyers want to pay slightly less than the last traded price, the bid side stacks up. If sellers rush in, the ask side grows. The intersection of supply and demand at many levels creates a detailed picture of value. Order books provide detailed data on price movements, which is essential for informed trading decisions. Market makers update orders constantly to reflect on new information.

Liquidity pools infer price from reserve ratios. In a constant product pool, the marginal price of token X in terms of token Y is y divided by x. When a trade happens, reserves shift, and the price adjusts. Pools track external prices indirectly through arbitrage. If the pool price deviates from other markets, arbitrageurs trade until the AMM price realigns.

Both methods work. Order books rely on explicit quotes. AMMs rely on implicit quotes shaped by arbitrage and user flow.

Although pools dominate DeFi spot swaps, order books have strengths that do not disappear.

For these reasons, centralized exchanges and some high performance decentralized platforms continue to maintain order books.

Modern DeFi traders often use DEX aggregators. These services query multiple pools and sometimes order book platforms, then split a swap across them to minimize expected cost. Some aggregators also interact with hybrid models that combine features of AMMs and order books for optimal execution. They consider:

Aggregators are one reason AMM-based exchanges handle large volume smoothly. They abstract away the need to understand every pool and connect to the best combination available.

Even with strong models, execution requires care. Security measures, such as using audited platforms and secure wallets, are essential to mitigate risks and maintain trust in trading. Use these practices to reduce cost and risk.

If you plan to provide liquidity rather than trade, keep these points in mind.

Use this quick decision framework:

Both models offer numerous benefits depending on user needs and market conditions.

What is the simplest way to understand order books vs liquidity pools

An order book is a marketplace of quotes from buyers and sellers. A liquidity pool is a vault of tokens that quotes prices based on math. Order books depend on humans or bots placing limit orders. Pools depend on an algorithm and on arbitrage to keep the price aligned with the rest of the market.

Why did early on-chain order books struggle?

Every order update is a transaction. On public chains, this is slow and expensive compared to a centralized server. As a result, the book was thin, spreads were wide, and trading felt clumsy. Liquidity pools avoided constant updates by using a formula that only changes when someone trades.

Do liquidity pools set prices fairly?

Yes, within the limits of their design. The formula sets a price from reserves at all times. If that price drifts away from external markets, arbitrage brings it back. Deep pools and active arbitrage make pools accurate and hard to manipulate.

What is impermanent loss?

Impermanent loss is the value difference between holding your tokens and providing them to a pool when the price changes. If one asset rises relative to the other, you end up with more of the weaker asset and less of the stronger one. Fees can offset this, but providers should understand the effect before depositing.

Can order books and liquidity pools coexist?

They already do. Many ecosystems offer both. Aggregators route orders to the best platform, and some protocols combine order book depth with AMM liquidity to improve execution.

How does an automated market maker handle very large trades?

The price impact rises with trade size because the reserves move. For very large trades, aggregators split the order across multiple pools or use a request for quote system that sources better pricing from professional market makers.

Are liquidity pools vulnerable to manipulation?

Pools can be targeted during very low liquidity periods or when a stale oracle feeds a protocol that uses pool prices. Healthy pools with active arbitrage and deep liquidity are resilient. Many designs integrate time weighted average price checks to reduce manipulation.

When should I prefer an order book?

If you need advanced orders, access to derivatives such as perpetuals and options, or you are executing very large size in a mature market with professional market makers, an order book is likely the better choice.

Order book trading: A market structure where limit orders from buyers and sellers are matched by price and time priority.

Liquidity pools: Smart contracts that hold token reserves and use an AMM to quote prices for swaps.

Automated market maker: The formula or algorithm that determines pool pricing, such as constant product or stableswap.

DeFi liquidity models: The various designs used for on-chain markets, including constant product AMMs, stableswap curves, and concentrated liquidity.

Traditional markets: Conventional financial trading environments, such as stock exchanges, that rely on order books and centralized exchanges. Traditional markets typically involve institutional market makers and specific structures for matching trades, in contrast to the decentralized and automated systems used in DeFi.

Cryptocurrency market: The overall environment for trading digital assets, including various models like order books and AMMs. The cryptocurrency market encompasses both centralized and decentralized trading systems, impacting market accessibility, liquidity, and the evolution of digital asset trading.

Spread: Difference between the best bid and best ask in an order book.

Price impact: Change in the quoted price caused by a trade against a pool or by consuming multiple levels of an order book.

Impermanent loss: The value shortfall that liquidity providers may face when the relative price of pooled assets changes.

Arbitrage: Buying an asset where it is cheap and selling where it is expensive to align prices.

MEV: Maximal Extractable Value, which includes profits earned by reordering or inserting transactions in a block.

Concentrated liquidity: A model where LPs allocate funds to a custom price range to increase capital efficiency.

DeFi markets chose liquidity pools because they fit the reality of blockchains. Pools do not need ultrafast matching engines, they allow anyone to supply liquidity, and they settle atomically on-chain. Order book trading remains essential in many contexts, particularly for complex instruments and very large orders. Rather than choosing a single winner, modern crypto markets use both and connect them with aggregators so that users receive the best available outcome.

Understanding the strengths and limits of each DeFi liquidity model will make you a smarter trader or liquidity provider. Use pools when you value permissionless access, composability, and predictable on-chain execution. Use order books when you need advanced control, deep professional liquidity, and low spreads in mature markets. With the right choice for each job, you will spend less on fees and slippage while taking only the risks you intend to take.

In conclusion, liquidity pools play a crucial role in the DeFi ecosystem by enabling decentralized trading and yield opportunities, but they also come with risks such as impermanent loss and smart contract vulnerabilities.

Bitunix is one of the world’s fastest growing professional derivatives exchanges, trusted by over 3 million users across more than one hundred countries. Ranked among the top exchanges on major data aggregators, Bitunix processes billions in daily volume and offers a comprehensive suite of products including perpetual futures with high leverage, spot markets, and copy trading. Users can trade bitcoin and other major cryptocurrencies on the platform, taking advantage of advanced trading features. Known for its Ultra K line trading experience and responsive support, Bitunix provides a secure, transparent, and rewarding environment for both professional and everyday traders. Bitunix Academy adds structured lessons so you can build skills while you trade.

Bitunix Global Accounts

X | Telegram Announcements | Telegram Global | CoinMarketCap | Instagram | Facebook | LinkedIn | Reddit | Medium

Disclaimer: Trading digital assets involves risk and may result in the loss of capital. Always do your own research. Terms, conditions, and regional restrictions may apply.